On Monday, the Detroit Pistons waived SF Josh Smith. An NBA team willing to waive a player who they owe $13.5M this season and the next two seasons, came as a large surprise to many within the NBA community. Shortly after making this move Stan Van Gundy, the Piston’s head coach and president of basketball operations, let the media know this was done “to give [Josh Smith] his freedom to move forward.” Although Van Gundy was referring to Smith’s freedom to join a NBA title contender, it turns out this move gives Smith the freedom to spend $1.3M however he chooses.

The financials behind the Piston’s waiving Smith.

The Pistons are under contract to pay Josh Smith $13.5M this season, $13.5M in 2015/16 and $13.5M in 2016/17. However, by waiving Smith and using the “stretch provision”, the Pistons will pay Smith the $13.5M owed to him this season and then will pay Smith the remaining $27M – to not play for the Pistons – over the next 5 years. Below is a comparison of Smith’s salary before and after the Pistons used the stretch provision on his contract.

How this move saves Josh Smith $1.3M.

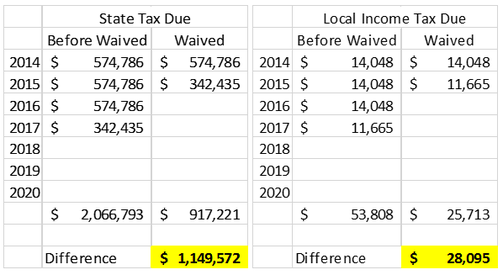

Professional athletes must pay state and local income taxes in each location they play. Tax authorities deem athletes to “earn” their income in the various NBA arenas they play each season. So, because Smith is being paid to not play, the income he will earn from the Pistons going forward will be “earned” in the state where he is a resident. Assuming Smith is financially savvy and lives in a state without an income tax, Smith’s salary (from the Pistons) going forward would be earned tax free in regards to state and local income tax. Looking at the tables below, we see what Smith would have owed in state and local income taxes before and after the Pistons used the stretch provision on his contract.[1]

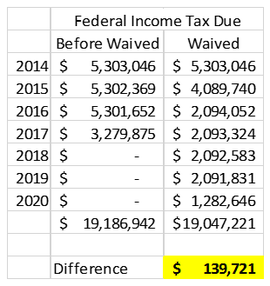

In addition to this move saving Smith millions in state and local tax, this move will save Smith some future federal income tax owed. Although Smith, like most professional athletes, would remain in the top marginal federal tax bracket regardless of being waived by the Pistons, the fact that our tax system is based on marginal tax rates will save Smith a little over $100,000 in future federal tax liability. By stretching Smith’s salary until 2020 instead of 2017, Smith will now be able to take advantage of lower marginal rates for three years he would not have originally been able to take advantage of. The table below details what Smith would have owed in federal tax before and after being waived by the Pistons.[2]

While it is highly likely Smith will sign a new contract with another NBA team for this season and possibly future seasons, the tax impact by his re-signing will be minimal. The income from the new contract will be subject to state and local income taxes in each location Smith and his new team plays. However, Smith will not be earning any of his old salary in those locations; he will only be earning his new salary in those locations. Therefore, his new salary – likely to be the veteran minimum of $1.45M – is what future state and local taxing jurisdictions will tax and not the $30M+ owed to him by the Pistons.[3]

RSS Feed

RSS Feed