No matter where you stand on the issue, it’s apparent that things are going to be changing in the near future for the NCAA.

On Friday, Judge U.S. District Judge Claudia Wilken officially published the latest blow to the status quo when she ruled in favor of O'Bannon and other plaintiffs by stating they should have been compensated by the NCAA for the likeness of their image.

While the O’Bannon lawsuit (or other legal actions against the NCAA) is far from over, NCAA athletes “playing” for free (or at least just tuition, room and board) appears to be over. Those athletes will no longer be “student athletes” but are now going to be paid employees for the services they provide their employers.

With their new status as employees, these athletes will now learn not only what it is like to be a professional on the field, but will face a new challenge off the field – state income taxes.

As we have previously discussed, taxpayers owe state income taxes in each state they earn income. For athletes who are compensated for their services – that means every state in which those athletes play. Until now, this was a headache only for professional athletes and limited to the various 20 states or so that hosted professional sports teams. Now, every state’s income tax policy will become a sales pitch by college recruiters to high school athletes across the country.

So, without further ado, the effect state income tax laws will have on college athletes.

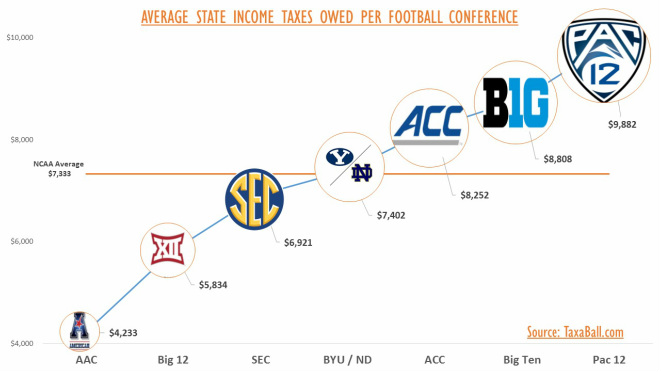

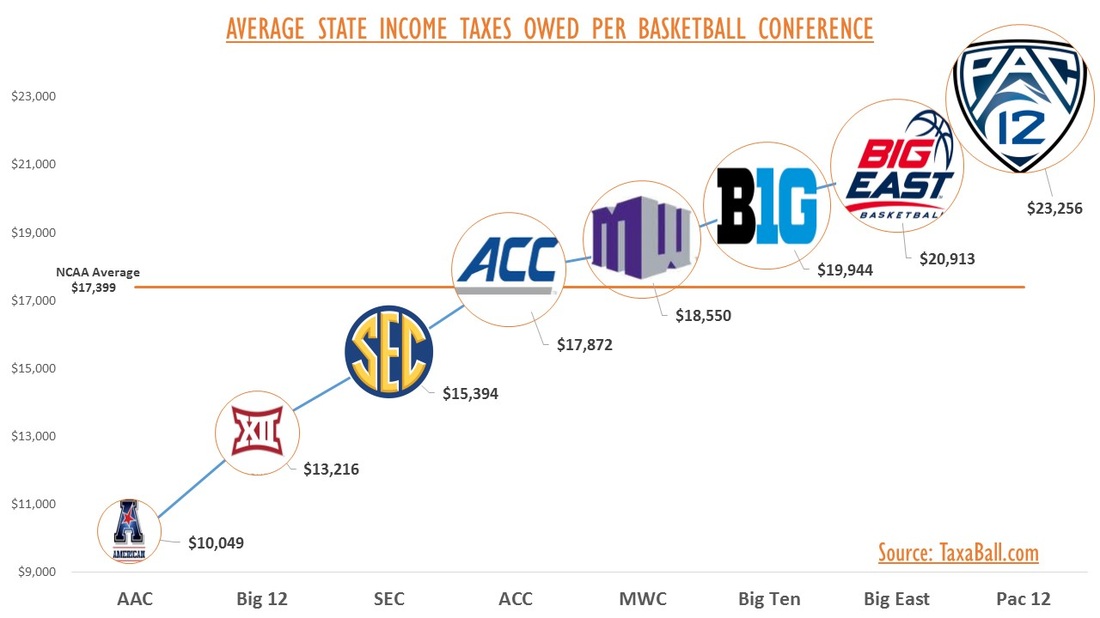

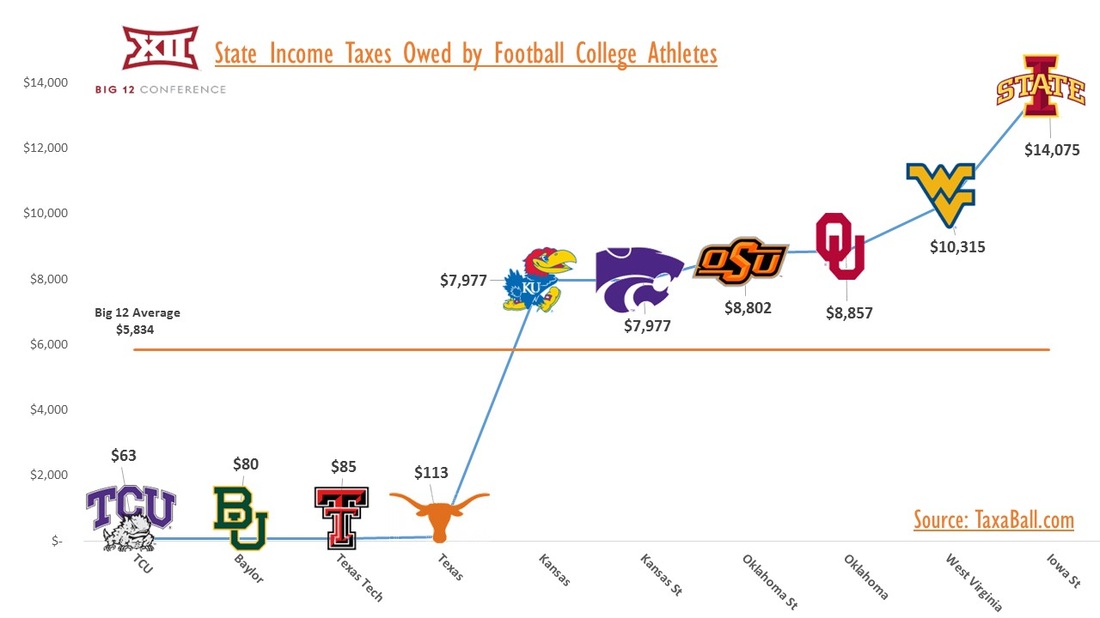

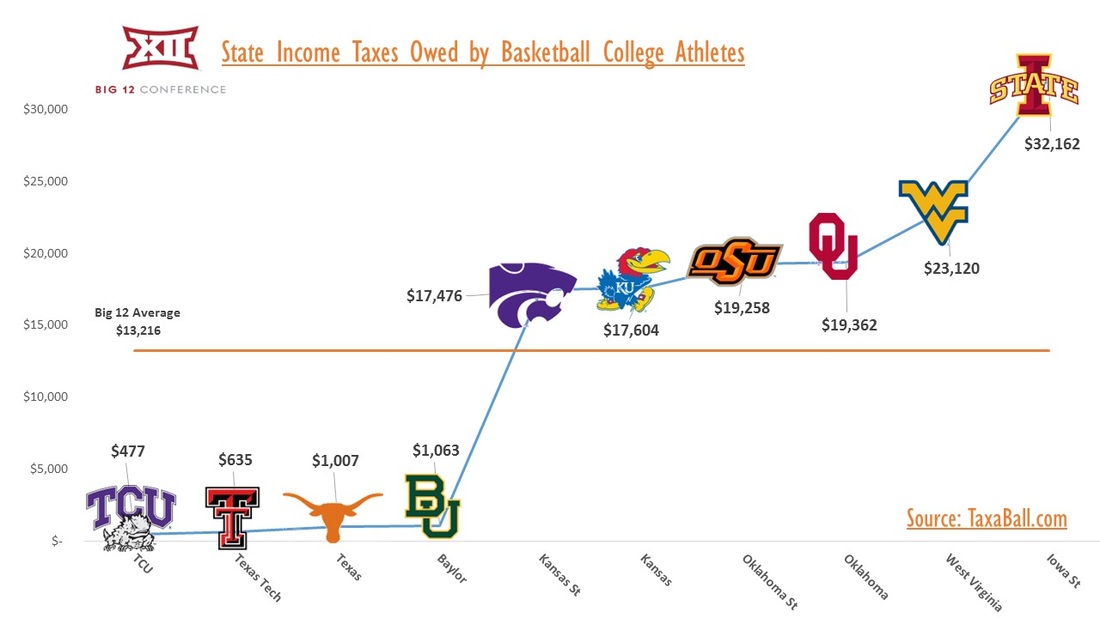

Using potential earning numbers for college athletes and applying those salary figures to the 2013 football and 2013-14 basketball schedules we calculated what a NCAA athlete would owe in state income taxes for each of the major football and basketball conferences’ schools. (Because last year's schedule was used, teams are assigned to the conference they were a member of during the 2013-14 seasons.)

On Friday, Judge U.S. District Judge Claudia Wilken officially published the latest blow to the status quo when she ruled in favor of O'Bannon and other plaintiffs by stating they should have been compensated by the NCAA for the likeness of their image.

While the O’Bannon lawsuit (or other legal actions against the NCAA) is far from over, NCAA athletes “playing” for free (or at least just tuition, room and board) appears to be over. Those athletes will no longer be “student athletes” but are now going to be paid employees for the services they provide their employers.

With their new status as employees, these athletes will now learn not only what it is like to be a professional on the field, but will face a new challenge off the field – state income taxes.

As we have previously discussed, taxpayers owe state income taxes in each state they earn income. For athletes who are compensated for their services – that means every state in which those athletes play. Until now, this was a headache only for professional athletes and limited to the various 20 states or so that hosted professional sports teams. Now, every state’s income tax policy will become a sales pitch by college recruiters to high school athletes across the country.

So, without further ado, the effect state income tax laws will have on college athletes.

Using potential earning numbers for college athletes and applying those salary figures to the 2013 football and 2013-14 basketball schedules we calculated what a NCAA athlete would owe in state income taxes for each of the major football and basketball conferences’ schools. (Because last year's schedule was used, teams are assigned to the conference they were a member of during the 2013-14 seasons.)

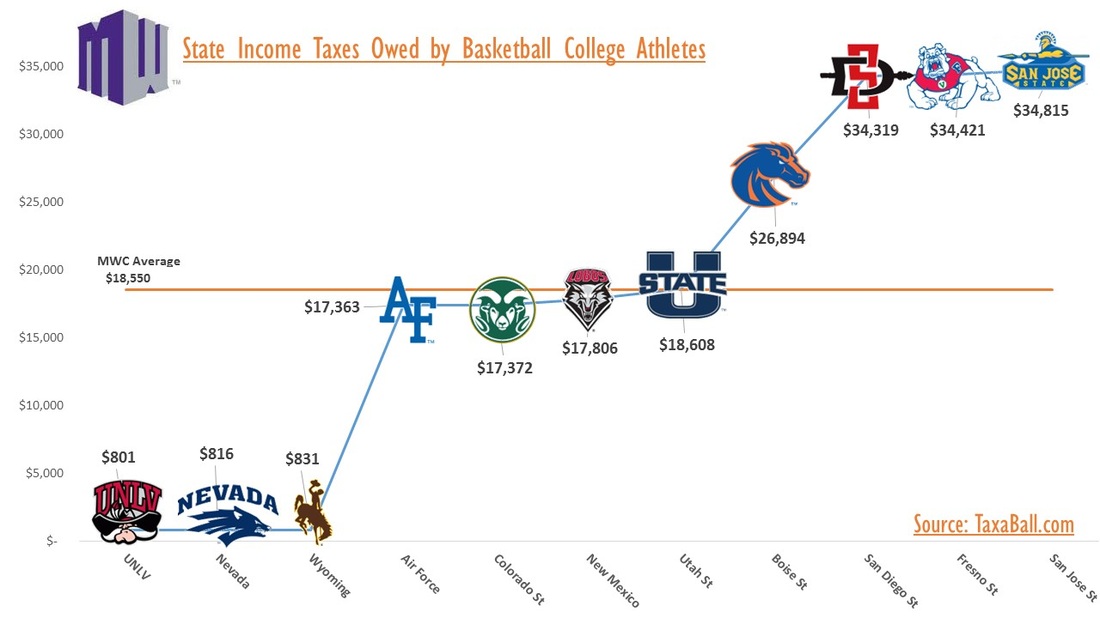

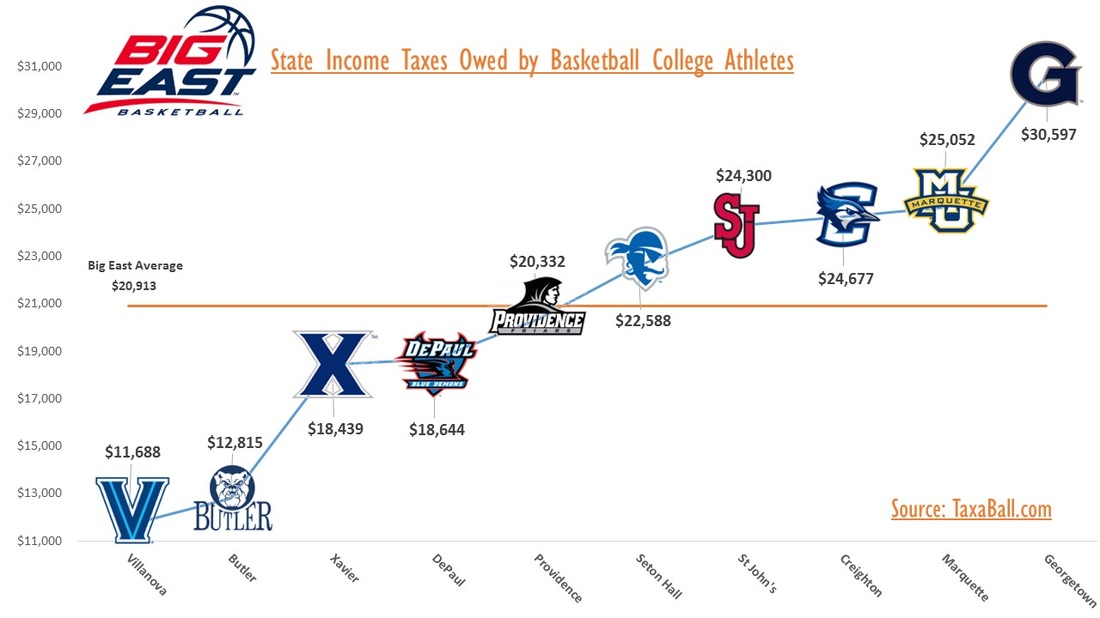

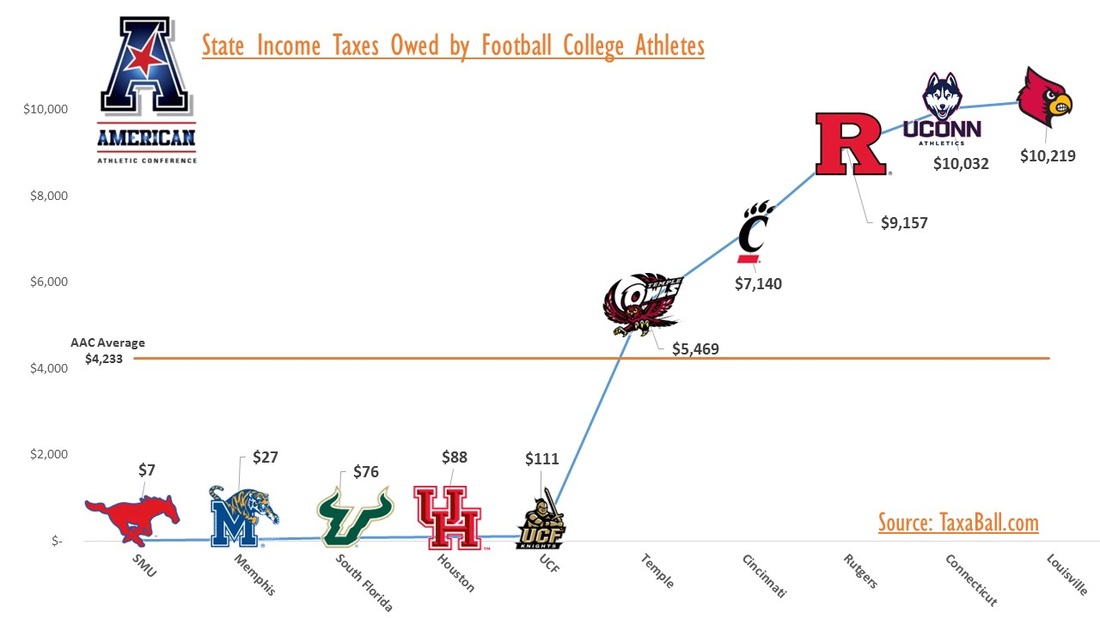

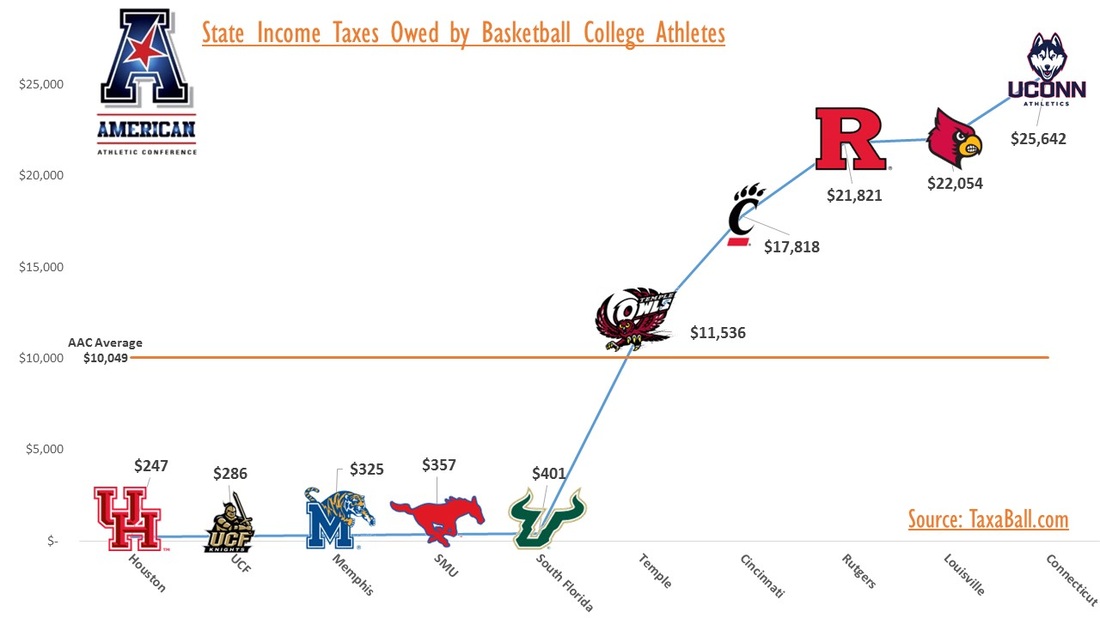

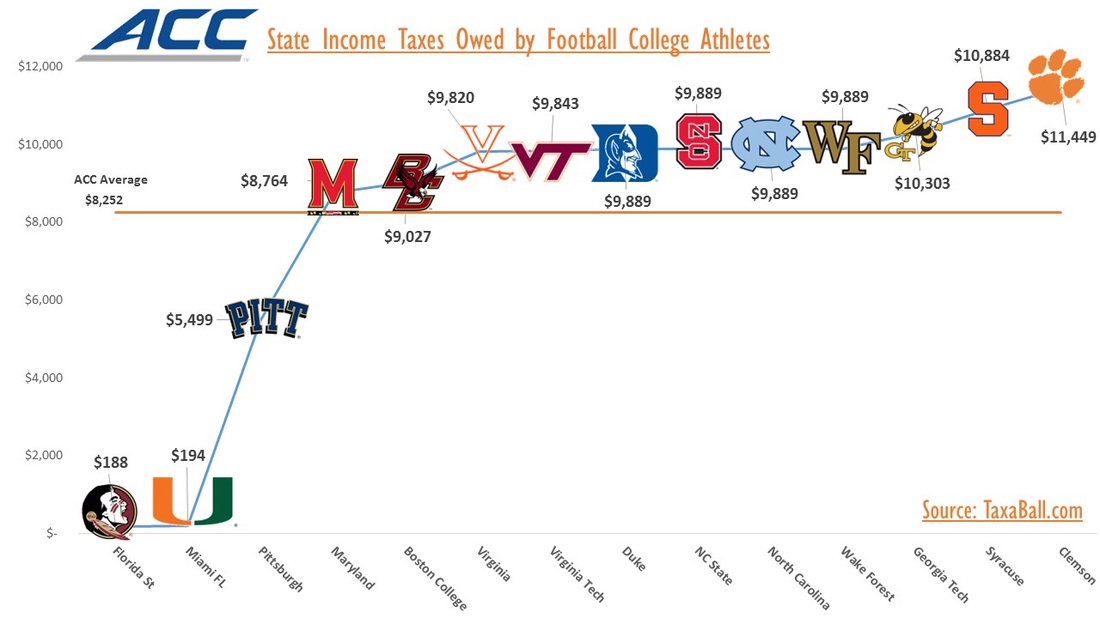

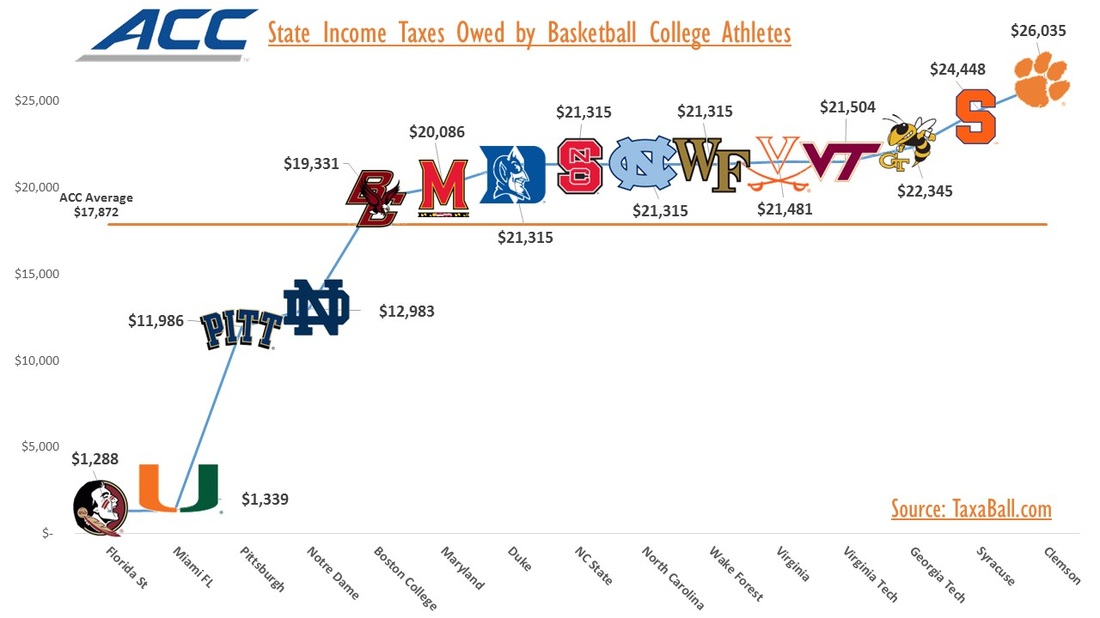

For the next several days, we will put out a team by team breakdown for each conference. Today is an overview of what the average state income taxes owed will be per conference. This is just the average for the conference so, as you will see in the coming days, this may greatly overstate or understate what a team in that conference may owe.

As can be seen by the graphics above, conferences that once appeared attractive to college athletes now may have to put some extra effort into their recruiting to convince a basketball player their school is worth $13,000 less in annual income or to convince a football player their conference provides enough benefits to outweigh paying double in state income taxes.

Be sure to check back throughout the week to see where each team ranks within their respective conference:

(NOTE: Some have misinterpreted this article as an argument against college athletes being compensated for their services. Nothing could be farther from the truth. Our intention is not to argue for or against college athletes being paid, that is an issue to be resolved by the courts. This article is purely intended to explain the tax implications once athletes are allowed to be paid.)

Be sure to check back throughout the week to see where each team ranks within their respective conference:

- Later Today: SEC (Football & Basketball)

- Tuesday: PAC 12 (Football & Basketball)

- Wednesday: Big Ten & Big 12 (Football & Basketball)

- Thursday: ACC & American (Football & Basketball)

- Friday: MWC & Big East (Basketball)

(NOTE: Some have misinterpreted this article as an argument against college athletes being compensated for their services. Nothing could be farther from the truth. Our intention is not to argue for or against college athletes being paid, that is an issue to be resolved by the courts. This article is purely intended to explain the tax implications once athletes are allowed to be paid.)

RSS Feed

RSS Feed